![]()

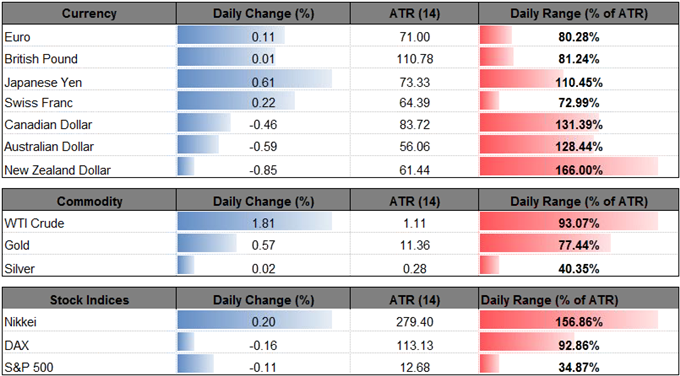

The Japanese Yen outperforms its major counterparts going into the last full-week of November, and USD/JPY may continue to give back the rebound from the 2017-low (107.32) should the Federal Open Market Committee (FOMC) Minutes drag on interest-rate expectations.

In light of the muted reaction to the 13.7% rise in U.S. Housing Starts, it seems as though market participants are still deciphering the fresh rhetoric from central bank officials especially as Dallas Fed President Robert Kaplan, a 2017-voting member, warns the 10-Year U.S. Treasury yield reflects pessimism for future growth. Even though the FOMC is widely anticipated to further normalize monetary policy in December, Mr. Kaplan noted that ‘prudent risk management means some action to remove accommodation gradually and patiently,’ and the FOMC may ultimately deliver a dovish rate-hike as the central bank struggles to achieve the 2% target for inflation.

With that said, a slew of cautious remarks from Fed officials may dampen the appeal of the greenback, with USD/JPY at risk of exhibiting a more bearish behavior ahead of the major U.S. holiday as the near-term outlook remains capped by the 113.80 (23.6% expansion) to 114.30 (23.6% retracement) region.

USD/JPY Daily Chart

![]()

USD/CAD extends the advance from earlier this week as Canada’s Consumer Price Index (CPI) narrows for the first time since June, and the pair may stage a larger correction over the remainder of the month as both price and the Relative Strength Index (RSI) preserve the bullish trends from September.

No Comments