Back in December 2013, we put “passive investors” in the Danger Zone for not recognizing that they are actually making active management decisions while skipping out on the due diligence of knowing what they own. We showed how it is practically impossible to make a “passive” choice given the sheer number of index fund options in almost every market segment. Moreover, there are wide holdings differences between funds that, according to their names, appear to be tracking the same thing. Judging by the continued flow of assets into passive index funds and ETFs, investors remain unfazed by these concerns.

Fund Flows to ETFs Continue Unabated

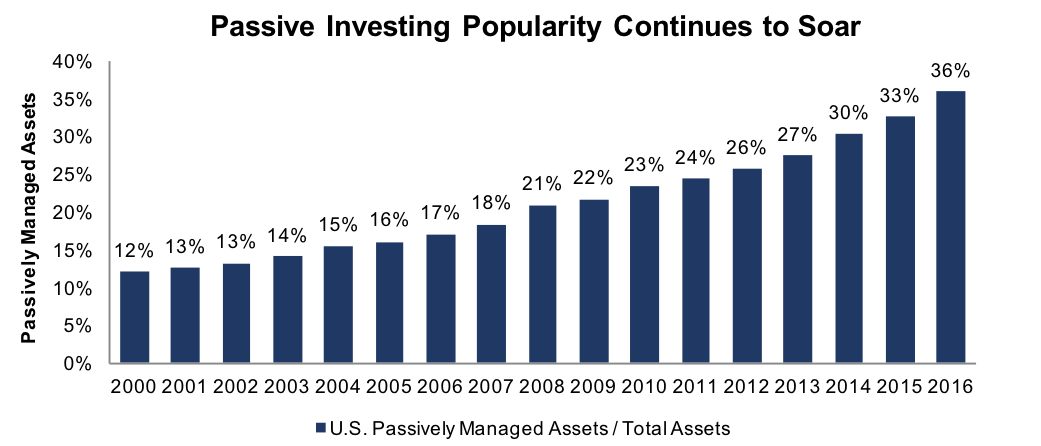

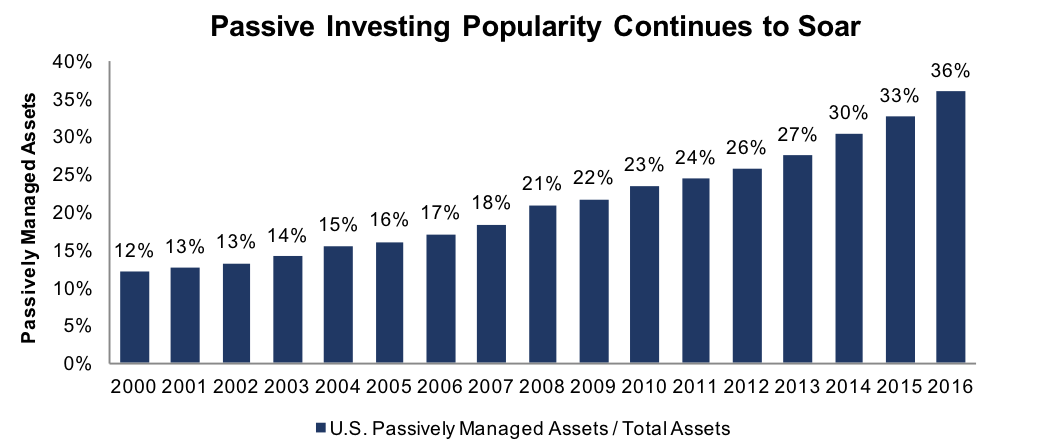

During 2016, actively-managed funds experienced $285 billion of outflows while passive funds attracted $429 billion of inflows. 2016 reflected the continuation of a trend that began during the Financial Crisis and has continued to build momentum. Disillusionment with Wall Street fund manager performance and an increasing focus on low fees remain the ostensible drivers. Since 2000, actively-managed mutual funds have seen roughly $1.5 trillion of outflows with ETFs capturing nearly all of it. The proliferation of ETFs is now approaching 2,000 funds and nearly $3.0 trillion of AUM.

Figure 1: Market Share of Passively Managed Assets Since 2000

Sources: New Constructs, LLC and Quartz (www.theatlas.com)

Thinking Through Potential Pitfalls

The ETF and passive investing proliferation has been widely heralded as a boon for small investors, primarily from a cost savings perspective. We agree in concept and state throughout our fund research (see here, here and here) that the only justification for fees above the ETF benchmark is “active” management that leads to out-performance. We remain cognizant of the potential for too much of a good thing, however, and are on the lookout for the second derivative effects and unintended consequences of the passive investing revolution.

There is no shortage of warnings in the marketplace on the dangers of the passive investing trend. Many such warnings come from those that have the most to lose: active fund managers. In an effort to help investors cut through the noise, we outlined our take on three risks we think bear watching and one that should garner the immediate attention of investment professionals (i.e. fiduciary duty):

No Comments