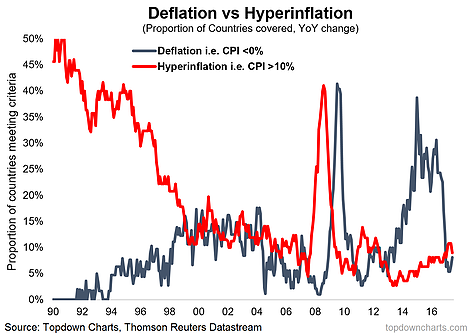

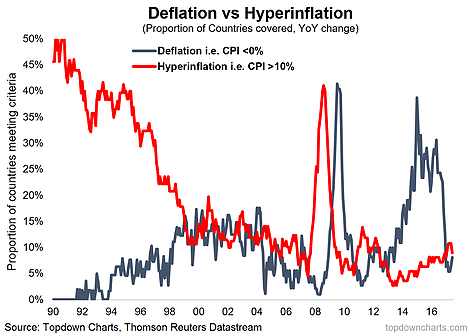

Recently the main talk in markets was reflation, but about 2 years ago everyone was talking about deflation: why deflation was structural, all the thematic aspects of deflation, and new normal and new paradigms. But in the end, it appeared to be cyclical or transitory – as the chart below shows. The chart shows the proportion of countries in ‘deflation’ (negative YoY change in headline CPI), which peaked about 40% in early 2015. The main driver was falling commodity prices, hence the transitory nature of it. But it was the largest, longest and most widespread episode of “deflation” that we’ve seen in recent history. Transitory or not, that kind of experience can have a big impact on investor psychology.

So in that respect it’s understandable that inflation expectations remain muted, with the deflation scare still lingering in investor minds. While inflation expectations have rebounded in Europe and America, there’s probably still at least 50bps of potential upside for both on mean reversion argument alone. Breaking down the components or drivers of nominal sovereign bond yields, inflation expectations are a key element and an uplift here would drive further upside in bond yields. The catalyst to drive repricing of inflation expectations may just be time – more time with no deflation. Overall though our view has been for a gradual move higher in inflation globally on the basis of better growth, shrinking spare capacity, rising property prices in the major economies, and stable commodity prices. Hence we remain tactically bearish on bonds and expect growth assets to outperform in the medium term.

After the peak of the deflation scare in 2015, there has been a sudden transition away from deflation. Is the next step a period of hyperinflation? (or at least higher inflation)

Inflation expectations remain below average, and a mean-reversion driven repricing could add further upside to bond yields. What’s needed for that is more time without the deflation that we just went through and a continuation of the trend of rising property prices, shrinking spare capacity, and stable commodities.

No Comments