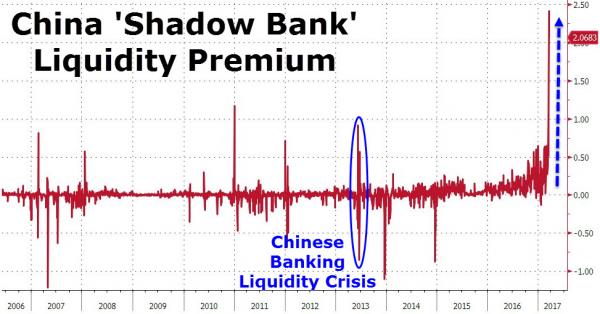

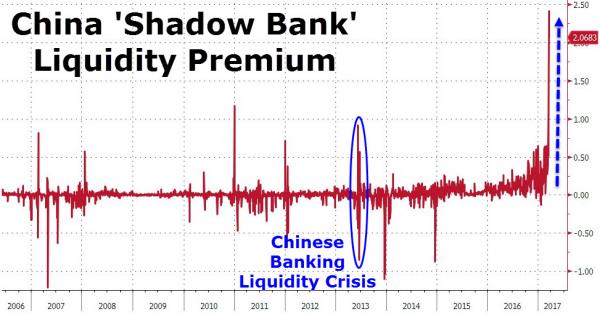

During the so-called Chinese Banking Liquidity Crisis of 2013, the relative cost of funds for non-bank institutions spiked to 100bps. So, the fact that the ‘shadow banking’ liquidity premium has exploded to almost 250 points – by far a record – in the last few days should indicate just how stressed Chinese money markets are.

While interbank borrowing rates have climbed across the board, the surge has been unusually steep for non-bank institutions, including securities companies and investment firms. They’re now paying what amounts to a record premium for short-term funds relative to large Chinese banks, according to data compiled by Bloomberg.

The premium is reflected in the gap between China’s seven-day repurchase rate fixing and the weighted average rate, which, according to data compiled by Bloomberg widened to as much as 2.47 percentage points on Wednesday after some small lenders were said to miss payments in the interbank market. Non-bank borrowers tend to have a greater influence on the fixing, while large banks have more sway over the weighted average.

“It’s more expensive and difficult for non-bank financial institutions to get funding in the market,” said Becky Liu, Hong Kong-based head of China macro strategy at Standard Chartered Plc. “Bigger lenders who have access to regulatory funding are not lending much of the money out.”

Without access to deposits or central bank liquidity facilities, many of China’s non-bank institutions must rely on volatile money markets. according to data compiled by BloombergThe People’s Bank of China has been guiding those rates higher in recent months to encourage a reduction of leverage, while also stepping in at times to prevent a liquidity crunch.

The PBOC responded to this week’s jump in borrowing costs by making an unscheduled injection of hundreds of billions of yuan on Tuesday, and it followed that with another addition of cash through daily open-market operations on Wednesday.

No Comments