Duke Energy (DUK) is a popular holding in many retirement portfolios because of the company’s generous and dependable dividend.

Duke Energy has paid uninterrupted dividends for more than 90 years and increased its payout each calendar year since 2005.

With a dividend yield above 4%, a high Dividend Safety Score, and low stock price volatility, Duke Energy is worth a closer looks.

Let’s review Duke Energy’s business and dividend profile to see if the company is a solid candidate for investors living off dividends in retirement.

Business Overview

Duke Energy’s history dates back to the early 1900s, and the company is largest electric utility in the country today with over $23 billion in annual revenue and operations reaching across the Southeast and Midwest regions.

Duke Energy is a regulated utility company that serves approximately 7.4 million electric customers and 1.5 million gas customers, including customers from its $4.9 billion acquisition of Piedmont Natural Gas.

Regulated electric utilities account for 89% of Duke Energy’s earnings, but the company also has a fast-growing gas infrastructure and utilities business (8%) and a commercial portfolio of renewables (3%).

Management sold Duke Energy’s international energy business (which was 5% of earnings) last year to reduce its earnings volatility and focus the company completely on its core domestic operations.

The company’s regulated utilities primarily rely on coal and oil (34%), nuclear (34%), and natural gas (28%) for its generation of electricity. Hydro and solar generate another 4% of the company’s total fuel.

Duke Energy continues investing in cleaner power generation (e.g. natural gas), which has helped reduce its fuel mix of coal and oil from 61% in 2005 to under 35% today.

Business Analysis

Many utility companies are essentially government regulated monopolies in the regions they operate in. Aside from in Ohio, all of Duke’s electric utilities operate as sole suppliers within their service territories, for example.

Power plants, transmission lines, and distribution networks cost billions of dollars to build and maintain in order to supply customers with power.

It isn’t economical to have more than one utility supplier in most regions because the base of customers is only so big relative to the investments required to provide them with electricity and gas.

Competition is further reduced by state utility commissions, which have varying degrees of power over the companies allowed to construct generating facilities.

However, the monopoly status of most regulated utilities has a major downside. The price they can charge for their services is controlled by state commissions.

This is done to keep prices reasonable for consumers while providing utility companies with enough of an incentive to earn a reasonable return on their investments made to provide safe and reliable service.

As a result, it’s very important to analyze the geographic regions that a utility company operates in. Some states have more favorable demographics (e.g. population growth) and regulatory bodies. Fortunately, Duke Energy plays in generally favorable regions.

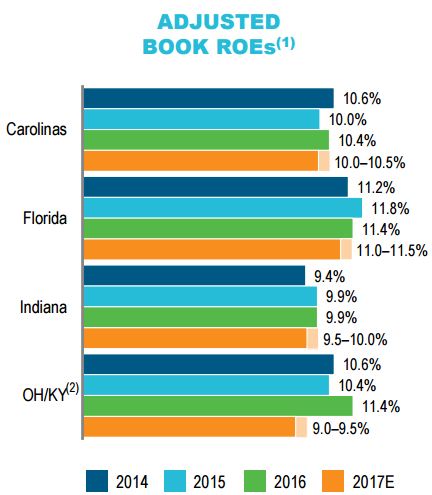

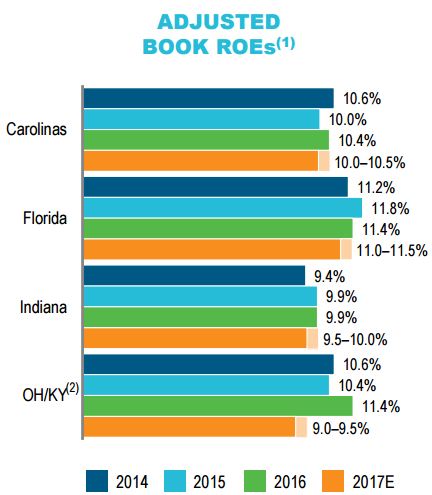

You can see that the company has earned a very stable and healthy return on equity between 9% and 11% in each of its regions over the last few years.

Source: Duke Energy Investor Presentation

These returns seem likely to remain stable over the coming years, in part because the rates charged to Duke Energy’s customers largely remain well below the nationwide average (only one of the company’s regions, Florida, charges a slightly higher rate).

This favorable differential should also make it easier for Duke Energy to win approval for higher rates in the coming years, supporting the returns earned by its ongoing growth projects.

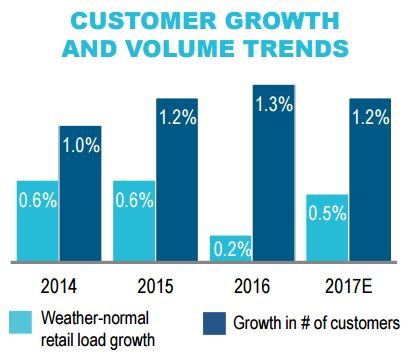

Customer growth also remains positive across the company’s regions, supporting a base level of retail load growth in Duke Energy’s large electric business.

Combined with the company’s cost management, this growth has helped support Duke Energy’s return on equity even without significant rate cases since 2013.

In addition to the favorable demographics and regulatory frameworks in its core markets, Duke Energy’s business has undergone a rather significant transformation over the last five years to improve the reliability of its earnings and cash flows.

Duke Energy’s biggest move was its acquisition of Progress Energy in mid-2012 for over $13 billion, significantly enhancing the company’s scale and market share in regions such as the Carolinas. Duke Energy has realized over $500 million in cost synergies from the deal and become a more efficient energy provider.

No Comments