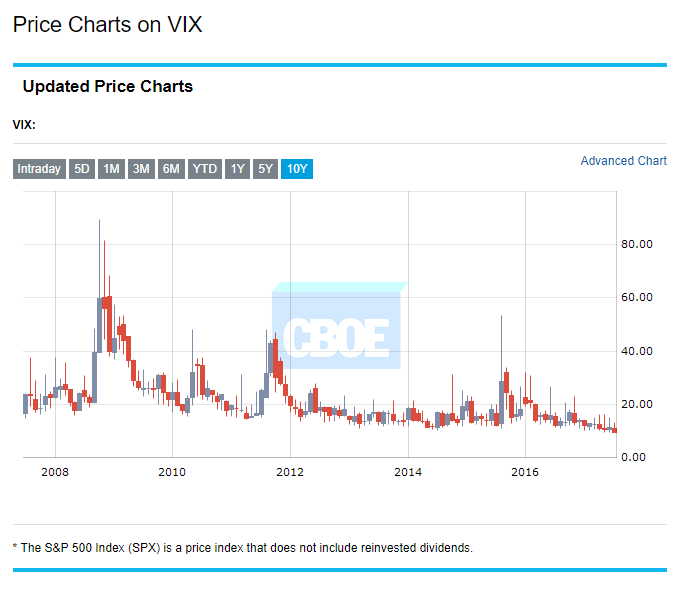

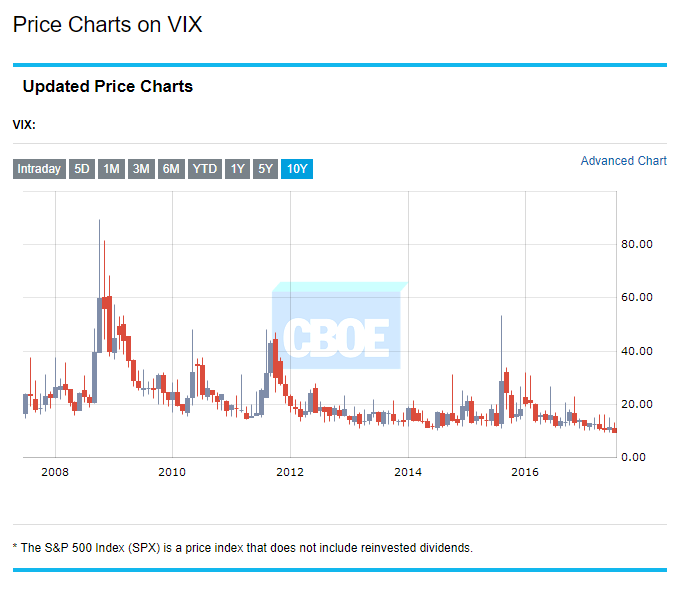

As Baupost’s President and Head of Public Investments Jim Mooney looks at the current volatility landscape, he uses a mathematical logic that considers the mechanics of how leverage impacts the risk management terrain. His logic (and likely that of his famous boss, Seth Klarman) is that statistically abnormal volatility – the CBOE VIX index was knuckle dragging near 9.50 in early Friday trading – leads to higher market leverage that is increasingly common to document as systematic, algorithmically driven strategies dominate markets.

It is at this intersection that Mooney – known in part for his skills at finding value after a market disaster as evidenced by purchasing Madoff claims after that complex settlement process – thinks he understands what is likely to be the next “accelerant” to the market crash. Leverage and systematic portfolio adjustments could exacerbate the rush to the exit whenever that seemingly inevitable event occurs, Mooney told investors in a Q2 Baupost letter reviewed by ValueWalk.

Baupost Letter – With algorithmic programs running markets as never before, this time it really could be different

Unlike the era where human emotions were more materially identified as performance drivers tied to market volatility, the historic implementation of algorithmic thinking into markets exposes a different decision-making process that could impact markets in very different ways. The next time volatility strikes, it could be different, and Mooney points to systematic factors to back up his thesis.

The current bout of low volatility is generally explained by several factors. “The most prominent explanation is that the low realized volatility, which results when asset prices march steadily upward with very few interruptions, naturally causes quantitative models to predict a continuation of subdued volatility, i.e. low implied volatility.” The formula leads to a model where low volatility begets lower volatility. The performance driver for these “dampened market fluctuations” is steady buying of stocks resulting from assets flowing into passively managed index funds, Mooney says.

No Comments