To be sure, we’ve seen all kinds of examples of spec positioning gone horribly awry this year and everyone knows stretched bets can be a contrarian indicator.

But just because it keeps happening doesn’t make it any less funny.

On Friday evening, we documented the latest (and probably the “last” as the rest of the short was almost invariably covered after Wednesday’s rate hike) chapter in the ongoing loonie bear saga. After going record short CAD in late May, bears were burned horribly and in the week through Tuesday, specs trimmed their net CAD short by 30,375 contracts to just 9,581.

Well, another fun takeaway from the latest CFTC data is this:

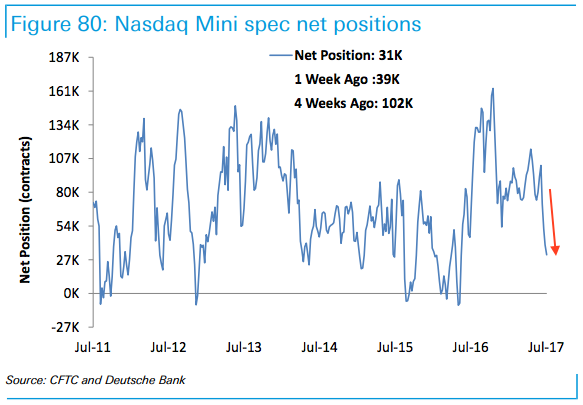

So that’s hedge funds cutting their net long positions in Nasdaq 100 futs for a 4th week in a row to just 31k contracts, the lowest since May 2016.

That is of course understandable. After all, tech began to have a rough go of it after a Goldman note out on June 9 spooked the market, leading directly to several weeks of tech underperformance.

At one point, the discrepancy between NDX implied vol. and S&P implied vol. was the most pronounced since 2002, a hilarious development considering the fact that the very issue Goldman flagged in the above-mentioned note was the extent to which tech had become synonymous with low vol.

So while it was rational to cut longs, it turned out to be a bad idea.

Because in the three days after specs cut their positions to the least net long tech since 14 months, tech stocks rallied 2.3% – the most since December 9.

No Comments