Image Source: Pexels

Image Source: Pexels

The FedEx (FDX – Free Report) disappointment likely has some company-specific aspects, but it is reasonable to see this report as providing a read-through for the broader economy that has shown signs of moderation lately. In fact, these signs of macroeconomic softness prompted the U.S. Fed to come out with a bigger interest rate than many in the market expected just a few weeks ago.FedEx missed on the top- and bottom-lines and guided lower, with several analysts covering the stock skeptical of the company’s ability to meet even the lowered guidance. Margins were under pressure as FedEx’s earnings declined -23% from the year-earlier period on -0.5% lower revenues. The company cited weak demand as a key driver of the earnings miss, but this factor is likely weighing on pricing trends as well.The FedEx report was for its fiscal first quarter that ended in August, which we and other data vendors consider part of the September-quarter tally. The results in recent days from Oracle (ORCL Quick QuoteORCL – Free Report) and Lennar (LEN – Free Report) were also for the companies’ fiscal quarters ending in August and, therefore, get counted as part of our overall 2024 Q3 earnings season tally. Of these two, the Oracle report was really impressive, with the company legitimately staking its claim as a notable player in the emerging artificial intelligence (AI) struggle.Including FedEx, Oracle, and Lennar, we have seen such early Q3 earnings results from 7 S&P 500 members, with another 7 index members on deck to report results this week. Costco, Micron, and Accenture are some of the notable companies reporting results. By the time the Q3 earnings season really takes the spotlight when the big banks start reporting their quarterly results from October 11th onwards, we will have such early results from almost two dozen index members.

The Earnings Big Picture

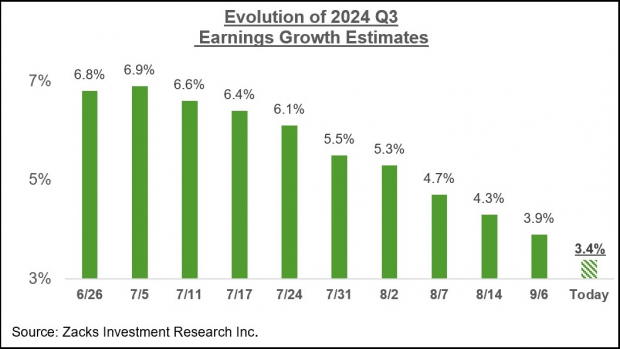

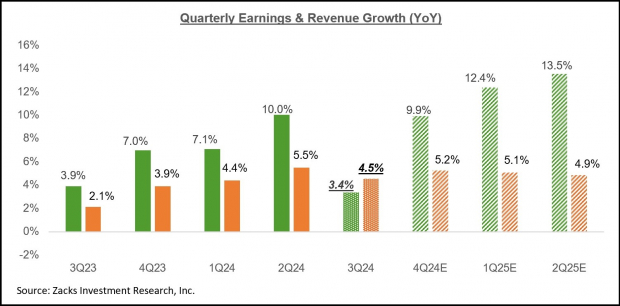

Total Q3 earnings for the S&P 500 index are expected to be up +3.4% from the same period last year on +4.5% higher revenues. This would follow the +10% earnings growth for the index in the preceding period on +5.5% higher revenues.Regular readers of our earnings commentary are familiar with our sanguine view on corporate profitability; the earnings picture isn’t great, but it isn’t bad either.The one recent negative development on this front is the reversal of the earlier favorable revisions trend that we have regularly flagged in our commentary. This negative revisions trend is particularly notable with respect to expectations for 2024 Q3, with earnings estimates for the period getting revised down a lot more than we had seen in other recent periods. You can see this in the chart below that tracks the evolution of Q3 earnings growth expectations over the last couple of months. Image Source: Zacks Investment ResearchNot only is the magnitude of cuts to Q3 estimates bigger than what we saw in the comparable periods for the last three quarters, but it is also widespread and not concentrated in one or a few sectors.Of the 16 Zacks sectors, estimates have been revised down for 14 sectors, with the Transportation, Energy, Business Services, and Aerospace sectors suffering the biggest declines. The Tech and Finance sectors are the only ones whose estimates have modestly risen since the period began.The chart below shows the Q3 earnings and revenue growth expectations in the context of what we saw in actual results over the preceding four quarters and what is expected over the following three quarters.

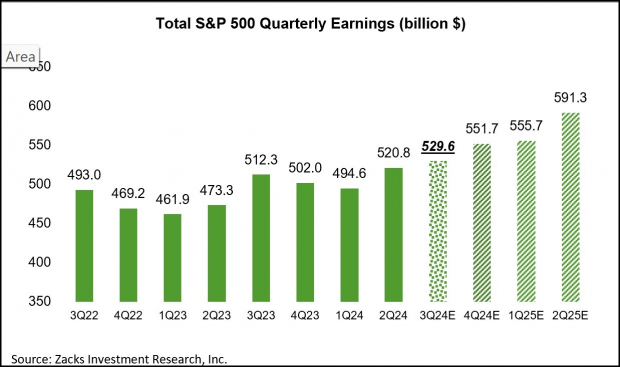

Image Source: Zacks Investment ResearchNot only is the magnitude of cuts to Q3 estimates bigger than what we saw in the comparable periods for the last three quarters, but it is also widespread and not concentrated in one or a few sectors.Of the 16 Zacks sectors, estimates have been revised down for 14 sectors, with the Transportation, Energy, Business Services, and Aerospace sectors suffering the biggest declines. The Tech and Finance sectors are the only ones whose estimates have modestly risen since the period began.The chart below shows the Q3 earnings and revenue growth expectations in the context of what we saw in actual results over the preceding four quarters and what is expected over the following three quarters. Image Source: Zacks Investment ResearchNotwithstanding the aforementioned negative revisions trend, the expectation is for an accelerating growth trend over the coming periods. Also, the aggregate earnings total for the period is expected to be a new all-time quarterly record, as the chart below shows.

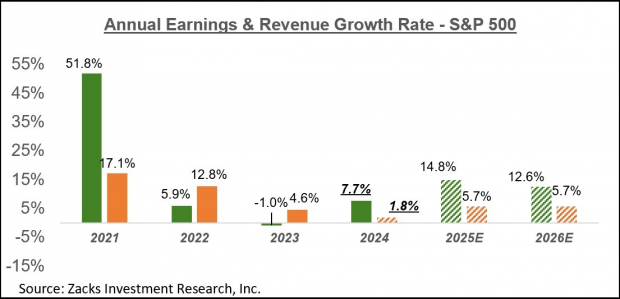

Image Source: Zacks Investment ResearchNotwithstanding the aforementioned negative revisions trend, the expectation is for an accelerating growth trend over the coming periods. Also, the aggregate earnings total for the period is expected to be a new all-time quarterly record, as the chart below shows. Image Source: Zacks Investment ResearchThe chart below shows the overall earnings picture on a calendar-year basis, with the +7.7% earnings growth this year followed by double-digit gains in 2025 and 2026.

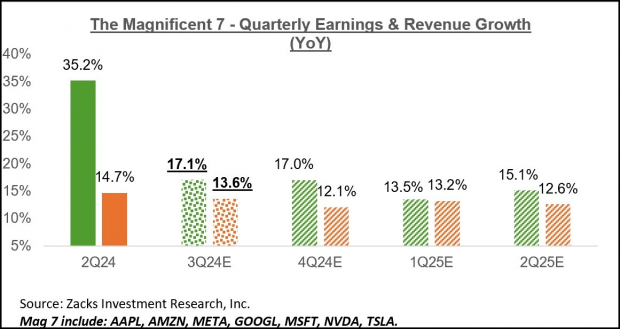

Image Source: Zacks Investment ResearchThe chart below shows the overall earnings picture on a calendar-year basis, with the +7.7% earnings growth this year followed by double-digit gains in 2025 and 2026. Image Source: Zacks Investment ResearchPlease note that this year’s +7.7% earnings growth improves to +9.6% on an ex-Energy basis.Expectations for the Magnificent 7 and the Tech SectorTesla will be the first Mag 7 company to report Q3 results on October 16th, with most of its peers in the elite grouping reporting in the following two weeks.For Q3, Mag 7 earnings are expected to be up +17.1% from the same period last year on +13.6% higher revenues. The chart below shows the group’s Q3 earnings and revenue growth expectations in the context of what we saw in the preceding period and what is expected in the coming three quarters.

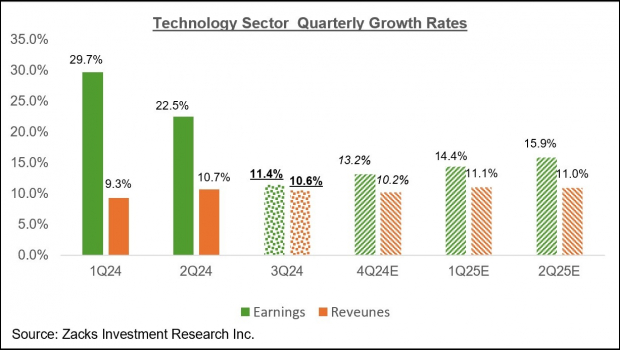

Image Source: Zacks Investment ResearchPlease note that this year’s +7.7% earnings growth improves to +9.6% on an ex-Energy basis.Expectations for the Magnificent 7 and the Tech SectorTesla will be the first Mag 7 company to report Q3 results on October 16th, with most of its peers in the elite grouping reporting in the following two weeks.For Q3, Mag 7 earnings are expected to be up +17.1% from the same period last year on +13.6% higher revenues. The chart below shows the group’s Q3 earnings and revenue growth expectations in the context of what we saw in the preceding period and what is expected in the coming three quarters. Image Source: Zacks Investment ResearchQ3 earnings from the Mag 7 will account for 21.4% of all S&P 500 earnings in the quarter. Excluding the Mag 7 contribution, Q3 earnings for the rest of the index would be essentially flat (up +0.2%).On an annual basis, Mag 7 earnings are expected to be up +30.7% this year on +10% higher revenues, with earnings expected to be up +16.2% in 2025 and +17.4% in 2026.Excluding the Mag 7, 2024 earnings for the rest of the S&P 500 index would be up +2.6% (+7.7% otherwise).For the Zacks Tech sector, Q3 earnings are expected to be up +11.4% from the same period last year on +10.6% higher revenues. The chart below shows the sector’s earnings and revenue growth expectations on a quarterly basis.

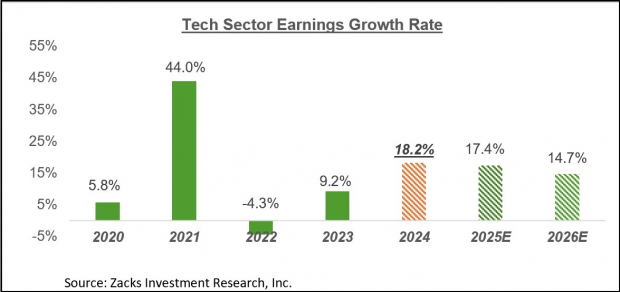

Image Source: Zacks Investment ResearchQ3 earnings from the Mag 7 will account for 21.4% of all S&P 500 earnings in the quarter. Excluding the Mag 7 contribution, Q3 earnings for the rest of the index would be essentially flat (up +0.2%).On an annual basis, Mag 7 earnings are expected to be up +30.7% this year on +10% higher revenues, with earnings expected to be up +16.2% in 2025 and +17.4% in 2026.Excluding the Mag 7, 2024 earnings for the rest of the S&P 500 index would be up +2.6% (+7.7% otherwise).For the Zacks Tech sector, Q3 earnings are expected to be up +11.4% from the same period last year on +10.6% higher revenues. The chart below shows the sector’s earnings and revenue growth expectations on a quarterly basis. Image Source: Zacks Investment ResearchThe chart below shows the sector’s earnings growth on an annual basis.

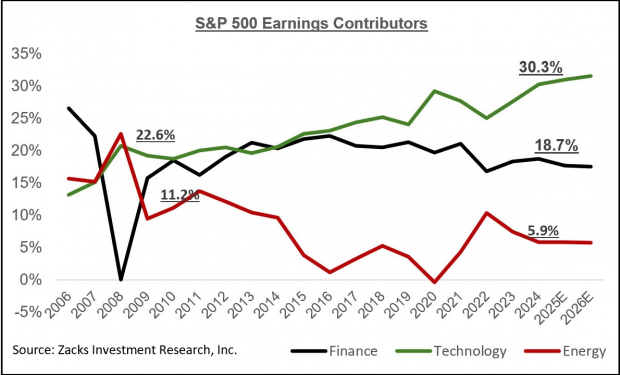

Image Source: Zacks Investment ResearchThe chart below shows the sector’s earnings growth on an annual basis. Image Source: Zacks Investment ResearchThe U.S. stock market is unique within the OECD group, as the Tech sector accounts for 39.1% of the S&P 500 index (by market capitalization). The sector is not only very profitable but also enjoying robust and sustainable growth momentum.The chart below shows the earnings contribution of the Zacks Tech sector relative to the same by the Zacks Finance and Energy sectors.

Image Source: Zacks Investment ResearchThe U.S. stock market is unique within the OECD group, as the Tech sector accounts for 39.1% of the S&P 500 index (by market capitalization). The sector is not only very profitable but also enjoying robust and sustainable growth momentum.The chart below shows the earnings contribution of the Zacks Tech sector relative to the same by the Zacks Finance and Energy sectors. Image Source: Zacks Investment ResearchMore By This Author:The Q3 Earning Season Gets Underway

Image Source: Zacks Investment ResearchMore By This Author:The Q3 Earning Season Gets Underway

Q3 Earnings: What Can Investors Expect?

What Will Q3 Earnings Season Show?

No Comments