The investment media is swirling with anxious prognostications about whether a recession and a Bear market in stocks are near. We received several calls and emails about that. Here is our opinion.

We are in a late stage of this market, perhaps in the 11th hour. The US stock market is historically expensive with significant valuation mean reversion risk. Earnings growth and margins are at high levels which also have significant mean reversion risk, with growing consensus that mean reversion of growth and profitability is not far away. However, few signs of an impending Bear market in stocks are present. Interest rates are still at low levels with the mean reversion process underway.

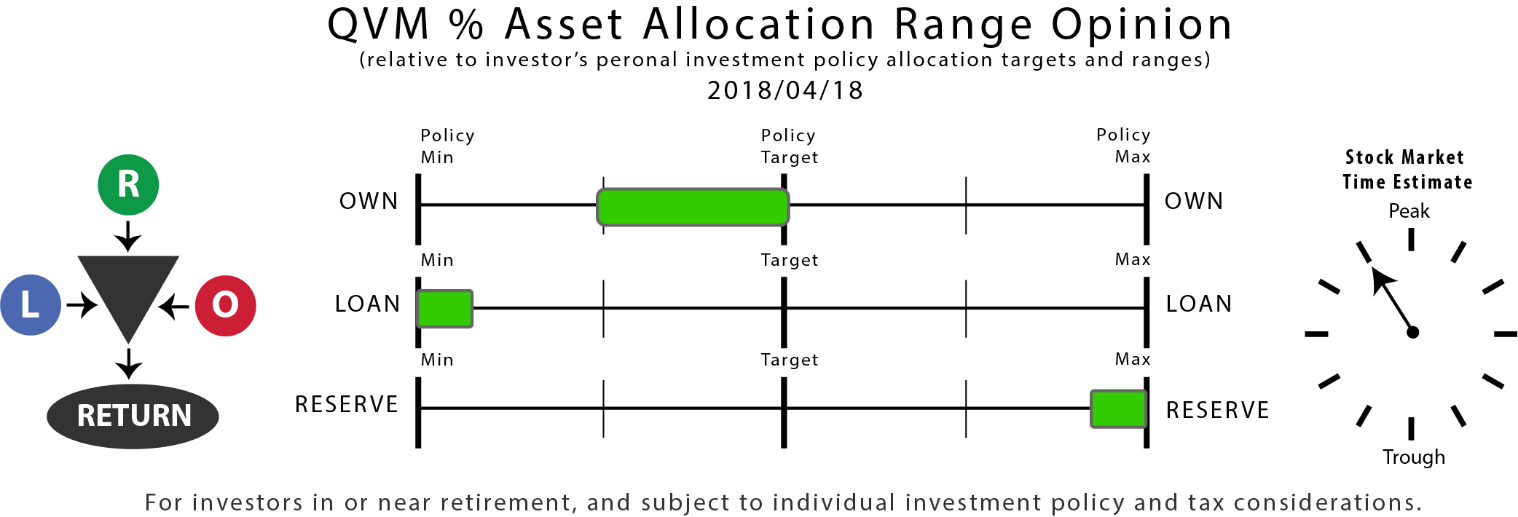

For investors who have substantially completed the asset accumulation stage of life, and are in or near the withdrawal stage, risk taking in stocks or bonds higher than long-term personal investment policy target levels is not prudent at this time. Maintaining equity exposure at or somewhat below the long-term target level is appropriate. Minimizing interest rate exposure in bonds is appropriate. Temporarily holding well above average near-cash reserves is appropriate.

For those planning tactical exits from stocks based on trend following, consider that more money has been made exiting stocks after a peak than before a peak. Stock markets can go on long past where skeptics expect them to fall. Predicting the peak is far less exact than recognizing the decline.

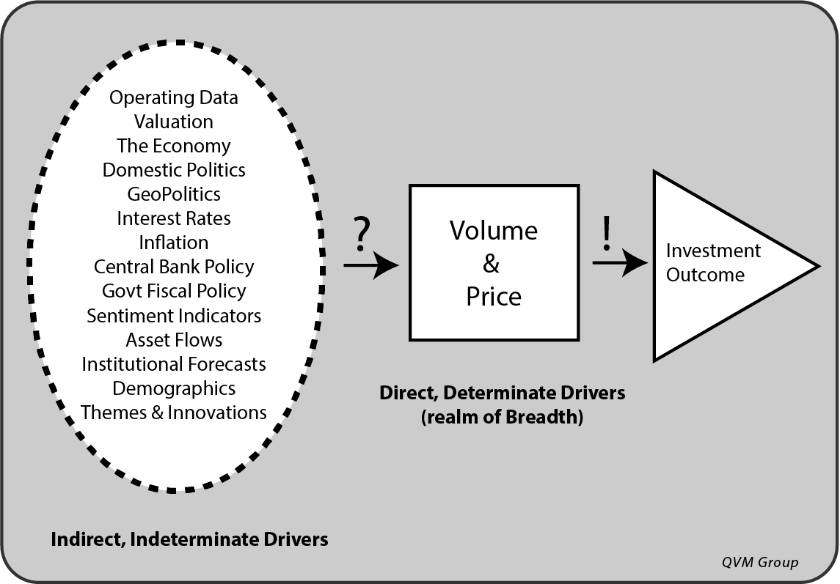

Breadth indicators suggest on balance that stocks are not ready to toss in the towel on the Bull. This is not based on company operating fundamentals, valuation, macro-economic factors, geopolitical factors, sentiment, asset flows, central bank monetary policy or government fiscal policy – all of which are important, but that in the end are all expressed in and through price and volume, which we are addressing with selected breadth indicators here.

Breadth measures how widely or narrowly market direction is shared among index constituents.

The Breadth Principle:

Breadth is important to monitor, because as more and more constituents move in the same direction as the parent index, the stronger the parent index trend direction, whether up or down. As more and more constituents fail to move in the same direction or move in the opposite direction of the parent index, the closer the parent index is to a trend direction reversal.

Behavioral Investing Risk:

We all tend to create a narrative based on what we think is important. Investors are swamped with information and biased to select the information that confirms their beliefs. How to filter and reduce information to effective action is a critical question. There is no “theory of everything”.

We tend to see what we want to see. But just because we are not looking for something, does not mean it’s not there.

Breadth helps narrow the information search. There are reasonable theories about breadth and forward market behavior.

Breadth is more quantitative and less prone (although not completely so) to show us only what we want to see than attempts to digest all available information. The market digests that information in the aggregate, but individuals cannot. In the end, all information reduces to price and volume behavior as final direct information. Breadth studies price and volume and assumes most of what it known has been factored into price and volume by the market.

No Comments